Unless you have been living under a rock for the last 10 years, you will have noticed that flash storage is growing - and it’s growing fast.

This is driven by reduced flash drive costs, advancements in software technologies and the increased performance required to run more agile businesses.

Initially flash storage was for specific applications, but the cost profile has changed and arrays are now being sold as mixed workload consolidation platforms.

Top 10 Disruptive Vendors

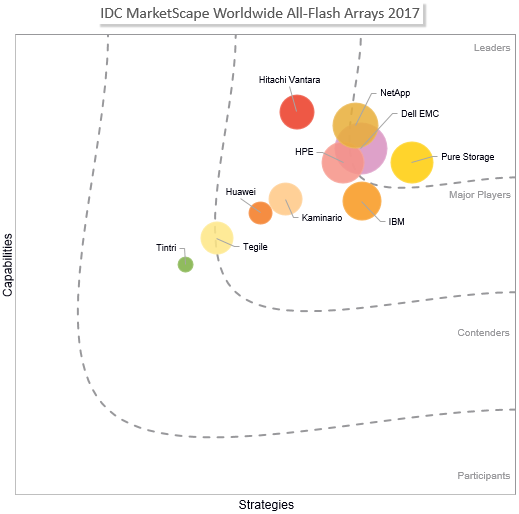

The chief report generators at IDC have produced a new report based on the market landscape for all flash arrays, focusing on 10 of the largest and most disruptive vendors in this arena: Pure, DellEMC, NetApp, HPE, IBM, Hitachi, Kaminario, Huawei, Tegile and Tintri.

The report focuses on two main elements, capabilities and strategies, the exact definitions can be found at the bottom of this post (see Further Reading).

Whilst these are two important factors, the report doesn’t take into account every factor possible and should be used as a way of short-listing vendors - rather than selecting a solution.

- Type 1: Arrays that were originally "born" as AFAs, think Pure, Kaminario etc.

- Type 2: These arrays originally began life as hybrid designs but have undergone significant flash optimisation and do not support HDDs. This could include HPE 3PAR StoreServ 9450 and 20850, and the Tintri EC6000 Series.

- Type 3: While beginning life as hybrid designs, these arrays have undergone significant flash optimisation - such as the Dell EMC VMAX All Flash and the NetApp All Flash FAS (AFF).

There are arguments as to why you should go for each type which I won't delve into. However, you should definitely consider which one suits you best.

Based on IDC’s number crunching they are expecting the split of spend for primary storage arrays to be 80% all flash and 20% hybrid or spinning rust arrays.

Does One Platform Fit All?

You may think that SSDs are end of it all, you would be wrong. We have NVMe, custom flash modules and virtual machine awareness, as well as more telemetry data than you can shake a high capacity hard drive at. The end of innovation is not here, in fact it is going to be a race that only accelerates over the time.

The platform that you choose for your organisation needs to be one that is not only good for your business today, but is being innovated upon.

Roadmaps are wonderful things, provided by vendors to woo you with features that at some point, in the next decade, could result in your new shiny toy. However, the market is driving these features to come out faster; the “start-up” vendors are no longer start-ups and are now a real threat to the established players.

Further Reading

If you want to read more on the report, Pure have an edited copy that you can download here.

We'd love to hear your thoughts on the world of storage; if you have a spare couple of minutes please participate in our survey. In return for your time you could win a Google Home device and a free on premise storage assessment!

IDC's Definitions

Current Capabilities: The platform's capabilities and menu of services, and how well aligned the vendor is to customer needs. The category focuses on the capabilities of the company and product today, here and now. IDC look at how well a vendor is building/delivering capabilities that enable it to execute its chosen strategy in the market.

Strategies: How well the vendor's future strategy aligns with what customers will require in three to five years. The category focuses on high-level decisions and underlying assumptions about offerings, customer segments, and business and go-to-market plans for the next three to five years.

- By Matthew Beale (Storage Solutions Specialist)